Author Archives: Charles Smith

Wise Company

Waste Management

West Irving Die

Woodward Governor

Younkers

Zeigler Coal

Zenith

Birds and the Bees About

Choosing Your M&A Investment Banker

If you are new to the game, heads up

Founder-owners of middle market companies usually only sell a company once in their life. The rainmakers at investment banks – the “closers” in Glengarry Glen Ross lingo – are skilled at getting new engagements. They pitch one deal after the next. They are polished at making a business owner believe that they are – and will continue to be – their banker. This is financial slight-of-hand to be aware of. Ask them if they will be your day-to-day contact during the life of the deal and watch their reaction and response.

The asymmetry in transaction experience between business owners and street-smart investment bankers leaves the owner vulnerable to the bait-and-switch gamesmanship of “closers”. Let’s lay out some of truths to be aware of before you give you heart to one of them.

Investment bankers only get paid for transactions that they either source or close. Bankers get paid a percentage of the value of their deals, not the firm’s deals. Since teams do not share their success fees with other teams, the financial motivation is to work on one’s own transactions and not assist other teams’ members due to the scarcity of time and other resources. It’s actually worse than just a lack of cooperation. Outperforming the guy next to them is their best path to partner. Because of that, bankers look left, then right, and then work to see that these interlopers are gone. Inter-team assistance is virtually non-existent as a result.

Rainmakers are motivated to sign up as many engagements as possible, not analyze companies. They want velocity, the quickest possible turnover so that they maximize their bonus. They have a financial incentive to get an acceptable price, not the highest price. The latter requires that they really roll up their sleeves and understand how your company will fit with each prospective buyer. That requires a lot of work. It also requires the next ingredient.

The vast majority of investment bankers have never been on the buy-side. They have never had to put together a set of financial projections they were held accountable for, never been involved in merger integration, never hired a CEO, and never had to turnaround a company. It’s hard to give sound advice if you’ve never actually been there, done that.

The person pitching you likely has not done any financial analysis for decades. Bankers that have survived at medium and larger firms are now managing people and client relationships. Their analytical skills have atrophied and they are dependant of the skills assigned to them out of the analyst pool. That makes for a quilt-work of the analytics the firm puts forth, and buyers see it. Their work is not integrated. Sections and paragraphs don’t fit together, and the reader is left to integrate the work themselves rather than being let to an inevitable favorable conclusion. Its like reading a version of The Old Man and the Sea where each chapter was written by a different college team rather than Ernest Hemingway. Its one of those things that hard to define, but you know it when you see it.

If your company is at or below the average size for an investment bank, they will assign junior people to your deal team to give them experience. Unless you are on the upper-end of the bank’s size range and value, you are likely to get “B” and “C” team talent. Being a Guinea pig or analyst trainer is not in your best interest. To get the best outcome, find a bank that specializes not just in your industry, but your size category. PE firms are very specific about the size of deals they will pursue. You need a bank that fits with your company’s size and the investment criteria range for the PEGs that match. The lowest end of the middle starts at $0.5mm in EBITDA and runs to about $2mm. Most lower middle market PE firm start at $2-3mm in EBITDA and run to perhaps $10mm. The majority are looking for double-digit EBITDA margins, so revenue expectations for this segment are roughly $10mm to $100mm. The middle of the middle market starts at roughly $10mm in EBITDA. Revenues at that point are $100mm and go up to $500mm where the upper middle market starts and our interest ends. Once a company hits $200mm in sales or better, it starts to have divisions that require separate diligence and pricing by the banker. Here is where a larger bank comes into play. Below this, it doesn’t help you. Each of these segments is distinct, with it own multiples that buyers are willing to pay due to the separate issues found in each size category. Typical EBITDA multiples paid increase as size increases. As a result, you can’t directly compare the EBITDA multiples paid for companies of different sizes. If your banker does so without adjusting for size, he is either incompetent or you are being mislead.

Bankers covet their buy-side relationships and resist sharing that relationship with other deal teams. Selling a company requires that they market the transaction to buyers where there is a fit. Also, bankers manage these buy-side relationships and have material relationship equity in them that they work hard to maintain. Try to sell a company to the wrong set of prospective buyers and they will put you on their spam list, stop picking up the phone, and terminate your hard-earned relationship. Because of the damage that can be done to a buy-side relationship, relationship bankers do not provide access to their buy-side clients unless it is in their personal interest. Bankers invest a significant amount of time and energy in developing their equity in these relationships. They simply do not permit access without a strong financial incentive, and then, provide access only with direct involvement and protection of the buy-side client.

Companies sell for different multiples depending on their size. This is because the smaller the company, the more numerous the likely weaknesses. These weaknesses include dependence on the owner, customer concentration, smaller geographic footprint, fewer deliverables or products, and a general absence of sophisticated talent acquisition and succession planning. When your banker shows you multiples for companies that are vastly different in size without an appropriate caveat, you are being conned.

Bankers will try to tell you your company is worth more than it really is to win the engagement. Every business owner wants to be told their business is worth a fortune. But a valuation in a pitch is worth exactly what you paid for it. Nothing. The banker has not conducted due diligence. They have barely scratched the surface at the time of the pitch. The hard truth is that even once a good banker has finished doing all their analysis and completed writing the information memorandum, they have still not completed due diligence. Only after the buyer completes their due diligence is the entire truth known. As a result, the earlier you are from that point, the wider the range needs to be to take into account all the possible outcomes.

All that matters is your deal team, not the firm. Think Seal Team, not Army Reserves. A smaller well trained, fast moving team will beat out a slower, larger, less well trained force. Due to the incentive comp, the only deal experience that matters, including industry experience, is that which belongs to your team members. Banks operate in discrete silos. If your banker tries to impress you with all the deals that his firm has done, ask him which ones he was the primary banker for. Watch the pupils dilate. Also, beware the bait-and-switch rainmaker. His job is business development. The more senior he is in the firm, the more likely he will not do any work on your deal after the engagement letter is signed. How important is experience? Entire investment banks have been created by a single rainmaker leaving a bulge-bracket firm with a deal team. Evercore, Greenhill and Moelis come to mind.

Lifetime experience matters. There is a reason that 35 year-olds aren’t running investment banks. They just don’t have the deal experience, credibility, and relationships that give them access to buyers. They can be good at running a group of analysts, but that is where it stops. As far as doing the negotiations in transactions, this is the purview of senior bankers. A good senior banker can just sense the situation. More junior people simply miss the queues. There are just too many tricks to the trade, and too many ways that a sophisticated buyer can take advantage of a first-time seller and less-than-senior team. Younger bankers operate out of their firm’s three-ring binder. This helps junior bankers, and they do well with plain vanilla, but if you need creativity and innovation, you need to find someone that has exhibited this during their career. Buyers are motivated to take advantage of color-by-number bankers, and whoever has the greater experience and creativity will win the day. Sun Tzu knew this well.

Most lower middle-market firms close relatively few transactions, and that is a good thing if you have “A” team talent and they are focused on you. The relatively small average number of transactions per firm (2-3)1 is due to the small number of team members needed to optimize the execution of the sale process of a lower middle-market company, from $2mm to $20mm in EBITDA. A deal team size of four is all that is needed. This includes one senior banker and his analysts and intermediate members. A full-time senior banker guides the team and, hopefully, is the ultimate analyst, writer, marketer, daily contact and deal guy. Experience counts, which leads us to our next point.

Investment banks are much like large law firms. Your corporate lawyer is really independent of the firm. The firm simply provides infrastructure. If your corporate attorney seeks counsel from another of the firm’s attorneys, that attorney bills for his time. As a result, attorneys operate within distinct and separate silos with your attorney working with his associates. Investment banking is the same. There are fairly famous examples of investment banks sprouting up virtually overnight due to a well-connected and regarded investment banker leaving a bulge-bracket firm with a deal team and setting up shop. Evercore and Greenhill are examples. Oh, and like the law firm, if you find that your attorney’s associates are the ones returning your calls, you’ve been assigned to the “B” team.

It is for these reasons we consider ourselves unique. We started on the buy-side. We were held accountable for our projections and ultimate outcome. WE had to compare projections to actual results for the life of the deal (doing this for a decade was a painful but enlightening experience). We had to fix our own problems. We sweated and worried and worked like madmen if things went South like they did in 1991. This pain caused learning that is irreplaceable. You cannot have empathy if you have not experienced the same pain. We have.

As a small firm that originated on the buy-side, we see things from your – and the buyers – point of view in a way other firms just can’t. We do our own projections using all past history and current competitor and industry information available, just like the buyer will. We personally possess control over each and every relationship with our buy-side clients. We do not have to consult with anyone before having contact with them. We personally control our human resources and dedicate them to a single transaction during the sale process rather than having them work on numerous transactions simultaneously. Unlike other firms which assign the work of a transaction to numerous low level analysts and then attempt to integrate the individual disparate parts, a senior banker conducts all analytical work and conducts all writing to ensure both accuracy and consistency in our work. We use our analysts solely for research, information acquisition, and formatting. Having been on the buy-side, we know what can go wrong. We’ve felt what you’ve felt. And having been there, part of our goal is to see you gain from the learning we’ve already paid for.

Footnotes

When to Sell Your Company

You have to know when to hold ’em and know when to fold ’em

The decision to sell your company is normally much more of a personal decision than an economic one. Owners need to have a personal reason to sell, like having something else they would rather do, like spend time with family, engage in a hobby, or address health issues.

Once an owner firsts thinks about selling, the next step is to think about factors unique to your company, the economy, changing technology, and your personal goals. Has it reached $5 million or more in sales? If so, it’s in the strike zone of many acquirors. If it’s still young and small, it has substantial risk, and you may be better off growing it to a size that diversifies the customer base and permits the creation of infrastructure so that a larger pool of buyers are attracted.

Where is your company on its growth and risk curve? Sometimes it makes sense to wait until growth starts to taper, so you can maximize profitability. Buyers will focus on a narrow range of EBITDA multiples that they will apply to your earnings based upon the size of your company. It’s important to get profitability as high as possible so that both numbers are at their highest possible level.

Then there is the health of the economy. Selling a company in 2009, or during any recession, isn’t the right timing. You always want to sell when credit is available to buyers, and your operating results are favorable. Market stability, measured by VIX, indicates a time of market calm.

Then there are your personal goals. Is there more you want to achieve from a personal gratification standpoint? Most of us entrepreneurs own our own companies because we have a passion. As long as that passion is in place, our health is good, we have balance in our life, have at least some wealth outside the company, and we don’t need the value inherent in the company for other personal or business reasons, then we should continue to enjoy what we do. The only caveat to that is if we really aren’t maximizing the value of the company and it would be worth more to someone else. Those situations do occur, and occur commonly.

The increasing rate of change in the world can blindside us, require us to re-engineer the company, or require skills, knowledge, or scale we don’t possess. Hiring the right talent goes a long way in bringing in fresh ideas. The entrepreneurs that survive long-term hire people smarter than themselves. Startups go through transitions, and if we’ve been fortunate enough to grow the company, there comes a time when we can’t do it all ourselves. To maximize the value of our companies, we have to make it self-sustaining, and able to live without us.

One of the best statements I’ve heard about raising children is that the goal isn’t to raise a good child. The goal is to raise a good adult. To do that requires that they can live without us, and many of us, at some level, are reluctant to let go. The same holds for our companies. If the company is dependent on us, it can’t possibly be at its best. Many private equity groups shy away from buying companies held solely by the founder. The PEGs have found that the founder holds on too tight.

We know an entrepreneur who has started and sold three companies and is now acquiring his fourth and fifth. The first three were ready to be harvested for one reason or another. The first two had started to see their growth and opportunities flatten out. The third met with changing industry conditions and he knew he was too small to compete, and he didn’t have the resources to make the acquisitions necessary to have the economies of scale to survive. So now he’s reinvesting in businesses with more defendable niches.

The easiest decision to make in the world of investment is the buy decision. The hardest is the sell decision. The exit planning process should start as soon as your company is operating successfully. When things have been really good, its hard to make the sell decision. But that is the best time to cash in your chips. Too many owners sell under duress, in the midst of a recession under very bad conditions. I’ve seen them walk away with nothing but a release of their personal guarantee where they could have retired a few years earlier quite wealthy.

Try to be as dispassionate about the sell decision as possible, and know that there are always other businesses you can reinvest in or other passions to pursue if the market is telling you its time to sell.

To learn more, write us at info@PegasusICS.com or click here

by Charles Smith

Mr. Smith is the founder of Pegasus Intellectual Capital Solutions, a boutique investment bank specializing in mergers and acquisitions, Capital Raising and restructuring and workouts. The firm is an innovator in the use of Intellectual Capital Audit for pre-closing due diligence and in turnarounds. Charles can be reached at csmith@pegasusics.comWhen to Sell Your Company?

Before the Recession of 2017/18

Our current expansion is well past middle-age and now eligible to join AARP

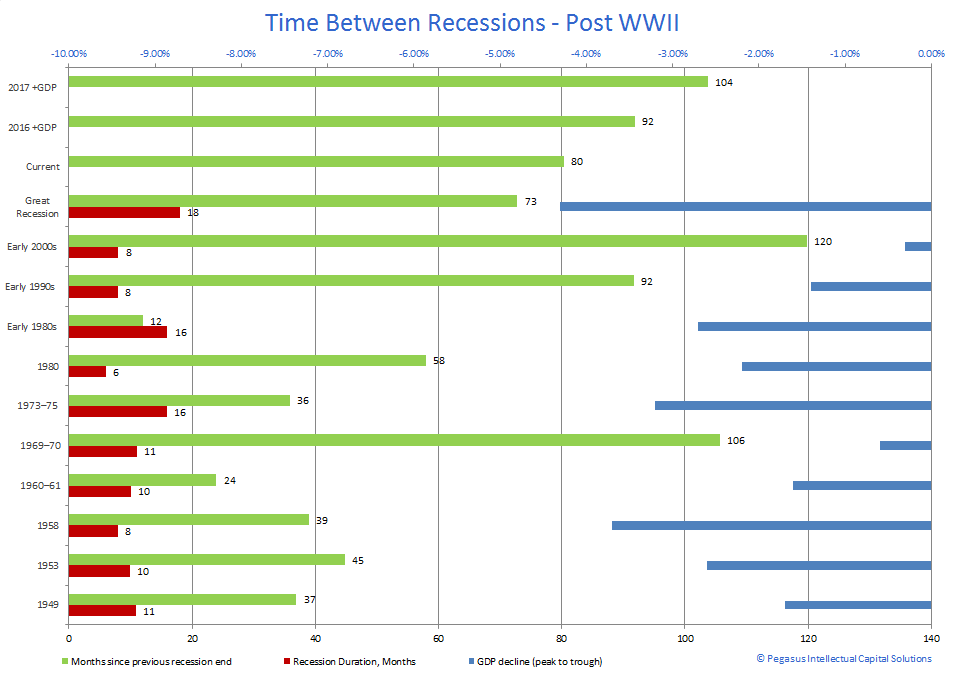

We’ve started to ask ourselves when the next recession will start. Our observation is that the M&A multiples are at – or a bit past – theirs prime for this business cycle. Also, banks seem to be having more credit problems. There is a rumbling among them that suggests they think it’s time to curtail the hell-for-leather business development mania that has been running its course the last several years.

It’s clear that our current economic expansion is past its prime and is now eligible to join AARP. At 80 months old, it exceeds the post WWII average of 60 months, as measured from the end of the previous recession.

Our sense is that 2016 will be okay, and so any recession must be in 2017 or later. In looking around the world, China is suffering a minor – if not larger – meltdown, putting downward pressure on commodity prices. As a result, all commodity related companies are marking-to-market their inventory, or kicking the can down the road by flowing above market cost-of-goods sold through their income statements thus deflating earnings. On the bright side, the consumer is the direct beneficiary. John and Jane Doe will put less dollars’ worth of gas in their car this summer and have more to spend on everything from eating out to taking a summer vacation. That’s why we think 2016 will be okay.

But we’ve also looked at CAPEX in O&G E&P; it’s down a third, and will lead to higher gas prices within 24 months, maybe less. Fracking wells play out in 18 months or so, so lower supply is looming. So, we looked at the length between the post WWII recessions, and extrapolated out our current expansion through this time in 2017, and then 2018.

Here’s the conclusion we drew based on some Kentucky Windage and simple observation: we look like we might have another 12 and 24 months of modest growth.

If we avoid a downturn for another 24 months, our expansion will be 104 months old. This will lag only 1st place winner of 120 months, and be nearly tied for 2nd place contestant at 106 months. This will still place it in the top 25 percentile of expansions.

We noted that the expansion that preceded the Great Recession was 73 months long (5th place), and we are at 80 now. We didn’t find that much of a comfort. The second longest post-war expansion was 106 months but it was followed by the stagflationary 1973-75 recession. This was a period of economic stagnation and high inflation in much of the Western world during the 1970s, which put an end to the general post-World War II economic boom. Again, we found little comfort in this.

While it’s possible that the Fed has found an anecdote to gravity, we have started to model a recession in 2018. In fact, we’ve almost started to hope for one. If we somehow eclipse the 120 month leader, we’ve begun to wonder what price we will pay.

© Pegasus Intellectual Capital Solutions

When to Sell Your Company? Watch the VIX 1

Going to market is like going to sea: do it while its calm

At some point, most business owners will ask themselves “When should I sell my company?”. This is important. Timing matters.

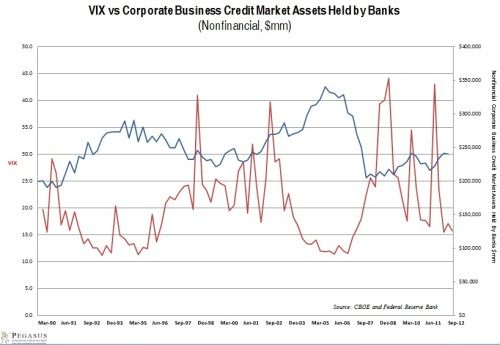

One of the articles I read recently was entitled “Banks Ride Business World’s M&A Wave”. That my caught my eye in addition to another, seemingly unrelated, article: “Fear Index Off Lows as Volatility Spikes”. My immediate thought was that mergers and acquisitions lending will fall in the near future.

It’s no secret that leveraged buyouts are big business with banks. Many of the larger banks have specialized groups, variously named, that handle the private equity groups that are behind much of the leveraged buyout lending. And there are of course the strategic buyers – every day companies – that also play in this market too. Both are plenty smart. Certainly smart enough to know when it’s time take risk and when it’s time to avoid it.

Our belief is that M&A lending has picked up because certainty has improved. What everyone had been looking has been some semblance of stability. The VIX option on the CBOE (domiciled here in our hometown, Chicago), is one of our favorite things to watch. Recently we looked for research regarding the relationship between stock market volatility and commercial lending activity. We didn’t find anything useful.

So we downloaded historical data on the VIX – the measure of statistical volatility of the S&P 500 – and Federal Reserve data on commercial lending activity to businesses (non-financial). Our work seems to indicate fairly clearly that a lack of volatility drives business lending activity. That should not be a surprise to anyone. The reason, we think, is quite simple: businesses hate uncertainty. That includes private equity groups, regular companies and Chief Credit Officers of the banks.

When the world looks uncertain, people don’t take risk. Buying a company is risky. Sales can fall by dramatic amounts (as they did in 2009) and you can lose your entire investment. The take-away for a business owner is that they should sell their company during a period of calm in the market. This will be an emotionally difficult decision for many business owners to sell, because who wants to get out when things are going well?

I know of too many owners who rode through the good times just to be forced to sell during bad times. Falling sales and faster falling EBITDA, covenant defaults, and forbearance agreements all cause serious damage to the market value of a company. Selling under duress is the worst of situations. About all you could add to that is failing health of the owner, and I have seen that as well. We sometimes see mourning families with all their net worth locked up in a leaderless company. Avoiding this is part of exit planning.

When you can, sit down with a piece of paper and write out when you intend to sell your company. What are the markers? I would suggest that you are still in good health, maybe 5-7 years from your intended retirement, your business is stable or positive, and banks are lending. You’ve achieved what you want from a personal gratification standpoint. And I would add at the end, the stock markets have low volatility as measured by the VIX.

You can see a current chart of the VIX here

If you’d like to learn more about mergers and acquisitions or exit planning, contact us at info@pegasusics.com.

(1) This article written in February 2013. In 2016, Harvard Law School published an article “The Real Effects of Uncertainty on Merger Activity” which confirmed our thesis about using the VIX as an indicator of market stability in predicting M&A activity

by Charles Smith

Mr. Smith is the founder of Pegasus Intellectual Capital Solutions, a boutique investment bank specializing in mergers and acquisitions, Capital Raising and restructuring and workouts. The firm is an innovator in the use of Intellectual Capital Audit for pre-closing due diligence and in turnarounds. Charles can be reached at csmith@pegasusics.comPreparing Your Company for Sale

Before hitting the launch button, go through the checklist

Preparing a company for sale – the M&A process – exit planning – entails a fairly extensive list of things that need to be done and considered. The process should start several years in advance of the sale process.

Among the many issues are:

– Succession planning, talent acquisition, training and talent retention

– Process review

– Diversification of risk

You will appreciate that most companies are purchased by private equity firms. To receive the highest possible price for your company, you need to be viewed as a platform company instead of an add-on. To be an attractive platform company, your company needs to have reached a stage where it sustains itself. It has Human Capital, Structural Capital and Relational Capital.

Put another way, it has good people, depth on the bench, and a process for recruiting, training and retaining them. It has internal processes that reflect an in depth understanding of the business in all respects including a strategy and a vision that extends out 5-10 years. And it has good or great customer and vendor relationships. In the absence of this self-sustainability, the buyer is really just buying your customer relationships, or technology, or some other part of the whole.

You – the current owner/operator – need to be expendable. Who is your replacement? Potential buyers want to know the company will survive once you leave. That requires talent acquisition, training, talent retention and succession planning. One of the challenges entrepreneurs have is letting go of the reins and bringing in someone that is their equal (or more than their equal). You need to have a real management team in place, with cross training of all your staff. There should be two people or more that know every job.

Preparing a company for sale should begin about a year or two year ahead of marketing the company for sale. Start with a review of all internal processes needs to be conducted. This is part of the due diligence a buyer will go through. They prospective buyers will ask themselves “Is the company as efficient and effective as it can possibly be using best practices and current technology?. If the company were being designed from the ground up today, is this the way you would put it together?” If not, look into the steps that can be taken in the next year or two and reflected in the financial statements the following year. Have you integrated current technology into your business processes? Software that increases efficiency is generally a good investment, even in the short-run. Related to this is where technology is headed, and whether the company has reviewed its strategic marketing plan to reflect the changing competitive landscape.

Diversification of your customer base is increasingly important given the rate of change in technology. Sales concentrations impair sales price and are an impediment to raising capital, as lenders are concerned about both uncollectable accounts receivable and unabsorbed overhead. One of the things that’s hard to predict is how changing technology will affect your customers. If you were dependent on Borders Book, or currently, Best Buy, anyone would rightfully be concerned about the outlook for your company. The best thing you can do is diversify your customer base, and watch the stock price of your customers. If they are public, watch their public competitors’ stock prices, and make this monitoring an integral part of your CFO’s job. There should be a natural tension between your CFO and Sales. If there isn’t, you don’t have balance.

These are some of the first things to think about in the process of preparing a company for sale. Exit planning is a job on top of your job, and we assume you are already fully employed. Talking to us when you being the process achieves two related goals. First, completing your exit plan. Second, we increase our knowledge of the company to a level where we can market it with greatest effectiveness. To learn more, contact us.

by Charles Smith

Mr. Smith is the founder of Pegasus Intellectual Capital Solutions, a boutique investment bank specializing in mergers and acquisitions, Raising Capital and restructuring and workouts. The firm is an innovator in the use of Intellectual Capital Audit for pre-closing due diligence and in turnarounds. Charles can be reached at csmith@pegasusics.comTo Sell Your Business, Start With The End in Mind

The path to wealth requires that you build a company that other’s want to buy… and pay a lot for.

The world of mergers and acquisitions is filled with sale transactions of middle market and lower middle market companies at prices well below what the companies would have been worth had the owner operated it with the intention to sell it from the beginning. Entrepreneurs make innumerable decisions along the way that did not maximize the value of the company in the eyes of its potential purchasers.

Decisions regarding choice of target market, customer concentration, R&D spending, hiring, compensation, succession planning, and systems are made that are expedient, easy, cheap or that simply didn’t look forward to a time when the owner would step down. Had the sale of the company always been planned for, most owners would have made certain decisions differently and worked to position the company as a leader in its field, ready to become a platform company for a private equity firm that could grow it through acquisition, using its structure as the foundation upon which they would build.

Regardless of how rational we believe we are, humans are subject to the whims of emotion. A recent article “Shopping Your Science”, Kuchner, Marc, The Scientist, April 2012 – outlined research that showed that people make purchase decisions using primitive pleasure and pain centers in our brain. With current brain scanning technology, we can see the center of the brain that lights up when an attractive object is shown to them. We can also see the pain center light up when a high price is shown. But comparing the size of the pleasure center with the pain center, researchers could predict whether the subject was inclined to purchase the object. What they concluded, is that all decisions, even purchase decisions, are emotional.

We can extend this pleasure-to-pain ratio to financial decisions by PEGs. If we have not prepared a company for sale, they perceive pain in the remaking of the company, with the associated uncertainty, effort, and stress that go into rebuilding the company.

One of the things we have learned in mergers and acquisitions is that it is very difficult to transfer the culture of one company to another as outlined in the article “Acculturation in Mergers and Acquisitions”, Nahavandi, Afsaneh, and Ali R. Malekzadeh, Academy of Management Review 13.1 (1988): 79-90. The “culture” is the way the company thinks, its values, how it does things, how it collaborates, who it hires, how it rewards. It is the summation of all of its attributes. Thus, those innumerable decisions that went into building your company are the determinants of your company’s culture. Its your secret sauce.

The culture of your company is the glue that binds it all together. If the company has critical mass, the culture endures after you are gone. Once established and codified in your Human Capital (HR), Relational Capital (sales/customers/suppliers). and operations policies and procedures, your culture continues after you exit. This is the part of the company that entrepreneurs commonly don’t build and the part of Enterprise Value they don’t obtain upon sale. Instead, entrepreneurs commonly sell the value of their customer relationships (Relational Capital), and likely they have pulled in some talented people, but have not created depth on the bench with succession plans for each key person, or created a talent acquisition and talent retention infrastructure that self-perpetuates. As a result, a PEG has a lot of work to do before the company becomes a real platform upon which they can grow both organically and through acquisition.

The question is, if succession planning and the creation of a self-sustaining culture are so important to the creation of the enterprise value of the company, why don’t entrepreneurs focus on it more intensely? The answer, of course, lies in the murky world of psychology.

Psychology is more important to mergers and acquisitions and exit planning that most entrepreneurs grasp. Humans are averse to certain thoughts, and among those are the aging process, failing health and death. Intellectually, we understand that we will get old, have health problems, and pass. But understanding something intellectually is not the same thing as understanding something emotionally. Our minds and our hearts often do not understand each other, even if they attempt to communicate, which they commonly don ‘t.

We have seen privately held business owners never plan for their retirement or hire and train their successor for taking the helm of the company. The consequence is often deleterious if not disastrous to the value of the company and those whom depend on the owner. “Key man risk” is all too common and is fundamentally a failure to conduct succession planning, which is central to building a company of enduring value.

The solution to maximizing the value of your company in a mergers and acquisitions transaction lies in conducting appropriate exit planning. By this we mean turning the company into a self-perpetuating going-concern. We do not mean tax planning for yourself or your estate, or anything unrelated to the company. Our focus is entirely on creating shareholder value. Taxes are high class problem we let other firms worry about.

If your company is established, regardless of how small or large it is, you will benefit from planning for your own succession and conducting exit planning. To learn more, contact us.

by Charles Smith

Mr. Smith is the founder of Pegasus Intellectual Capital Solutions, a boutique investment bank specializing in mergers and acquisitions, Capital Raising and restructuring and workouts. The firm is an innovator in the use of Intellectual Capital Audit for pre-closing due diligence and in turnarounds. Charles can be reached at csmith@pegasusics.comMaximize Shareholder Value,

Prepare for New Technology

The first digital camera, invented in 1975 by Kodak

The year 2012 has seen two famous companies collide with the Knowledge Era. Kodak was dropped from the Dow Jones average in 2004 and filed for bankruptcy in January 2012. In March 2012, The Encyclopedia Britannica announced it would no longer produce a print version.

But Apple, once on its knees, is the most valuable company in the world. As late as March 2003, its stock price was a meager $7.01 compared to its recent close at $542.83. In March of 2003, Kodak was trading at about $28.00, compared to its recent price of $0.21.

So why the difference in fates?

We can all blame Gordon Moore, the Intel engineer, and Moore’s Law: integrated circuit speed doubles every year (now 18 months). Some of us understood it, and some of us didn’t.

You may rightfully ask, what does this have to do with me? The answer is, if you are a business owner, an understanding how Moore’s Law will affect your business will affect the value in a mergers and acquisitions transaction and in your ability to raise capital. It will also determine your resistance to financial distress.

In 1975, Steven J. Sasson, one of Kodak’s research scientists, developed the first working model of the digital camera. It was met with doubts and questions from management. Moore’s Law was understood by Sasson, and he projected that in 20 years the technology would exist to create a digital camera with the storage and resolution that would make it a viable competitor to film.

But Kodak management couldn’t envision how consumers would use and share photos on their TV. The TV, or course, was the only viewing device for a digital photo of the era. And the TV was hampered by its own problems with resolution. High definition and 1080P were concepts yet to be created. Besides, Kodak saw themselves as inventing and selling coatings for films.

A line from Kodak’s internal report sums it up ““The camera described in this report represents a first attempt demonstrating a photographic system which may, with improvements in technology, substantially impact the way pictures will be taken in the future.” But, as they now acknowledge, they had no idea.

The playback device for the first digital camera: the TV. Its all executive management could envision.

Kodak had made two critical mistakes. Had they avoided one or the other, they might be prospering today.

– They put the digital camera and its patents back in the Warehouse of Lost Knowledge and promptly forgot it was there, just like the Arc of the Covenant being rolled back in the government warehouse in that unforgettable scene from the 1981 film “Raiders of the Lost Arc.”

– They defined themselves incorrectly: Fuji Film was in a very similar situation as Kodak. So why did they not meet the same fate? It defined itself differently. In its culture, it made chemical coatings, not film. It simply transitioned to coating other products, and used the same research engine.

And the first digital camera – and its patents – were rolled back into the warehouse of lost knowledge.

Encyclopedia Britannica had advance warning that it needed to change. Encyclopedias first came out on CD in the early 1990’s, and CD’s could be searched. But salesmen ran the company, and without their sales commissions for selling a print edition, they couldn’t see what other business model would benefit them personally. And so the company has become a shadow of its former self compared to the free and collaborative Wikipedia.

But what about Apple?

When Steve Jobs first initiated the R&D to develop the iPad, the technology didn’t exist. But Jobs foresaw that Moore’s Law would bring integrated circuit size and cost down to the place where he could make his wafer thin device technologically possible and economically affordable. By the time R&D was completed, integrated circuit size and cost had shrunk to a fraction of its former self, and a star was borne. Now the retailer Kohl’s plans to dispense with its cash registers and use only iPads due to their far greater number of applications.

Neither Kodak or Encyclopedia Britannica could see that the world was changing and would obsolete their way of delivering solutions to their customers. The customer needs still existed, of course. But the way of satisfying them are hardly recognizable. Photos and videos are taken from one’s cell phone, sent by text message to friends and family and uploaded to YouTube and Facebook. All information is at your fingertips at Wikipedia, which is one of the most visited, collaborative, and authoritative sites on the internet.

Things will get tougher in the next twenty years as the exponential improvement described by Moore’s law ultimately leads to the possibility of a technological singularity: a period where progress in technology occurs almost instantly.

A technological singularity is the theoretical emergence of greater-than-human superintelligence through technological means. Since the capabilities of such intelligence would be difficult for an unaided human mind to comprehend, the occurrence of a technological singularity is seen as an intellectual event horizon, beyond which events cannot be predicted or understood.

Computing speed will eventually collide with the rest of the corporate world.

Proponents of the singularity typically state that an “intelligence explosion”, where superintelligences design successive generations of increasingly powerful minds, might occur very quickly and might not stop until the agent’s cognitive abilities greatly surpass that of any human.

So, if Kodak had a hard time as early as 2004, and Encyclopedia Britannica started to struggle in the mid-1990’s, what exactly is going to happen to the rest of the corporate world and how do they prepare for it?

Corporations need to create off-site tech groups in Silicon Valley or in the Biotech world to protect their creative people from any corporate culture that prevents a rethinking of how things are done and why they are done a certain way. The creative, contrarian people are hard to manage by definition, and our Human Capital departments will need to make a place – a protected place – for them in the corporate environment.

Companies will need to white-board virtually constantly. When they wake up in the morning, the first thing they will need to ask is what changed overnight. They will need to create challenger teams that do nothing but come up with ways to obsolete and defeat everything the company does now, much the way Top Gun uses experts in our enemy’s methods and equipment to attempt to defeat our best pilots.

Collaboration will become more important than ever. No one person, or a single board or executive team will be able to assimilate all the information necessary to stay abreast of the changes unfolding. Corporate cultures will need to be designed to provide for the fluid exchange of information in all directions.

Whereas information has historically only traveled upwards in our Command and Control corporate cultures, those that survive will ensure that knowledge is exchanged downwards and sideways. This will run counter to the cultures of many companies, and the a Human Capital function will need to select for people that have the willingness and ability to share information freely and not control it.

In the world of finance, those companies that disclose that they are preparing for the future (without giving away their secrets) will enjoy a lower cost of capital, higher stock prices, have an easier time capital raising, enjoy higher mergers and acquisitions values and, and avoid financial distress.

As a result of all of this, the the Human Capital function in companies will become more important than ever. The selection and training of informed, collaborative people that freely share information will be central to a company’s ability to survive and prosper in an environment where progress in technology occurs almost instantly. To learn more, contact us

by Charles Smith

Mr. Smith is the founder of Pegasus Intellectual Capital Solutions, a boutique investment bank specializing in mergers and acquisitions, Capital Raising and restructuring and workouts. The firm is an innovator in the use of Intellectual Capital Audit for pre-closing due diligence and in turnarounds. Charles can be reached at csmith@pegasusics.comIncreasing Your Company’s Value:

It’s About Long Term Vision – and Helping Others

Shareholder Value Maximization is about long term value creation, not short term results, and that means investing in Intellectual Capital.

Maximizing the value of our company is about helping others, not just ourselves. The net worth of a business owner increases right along with the value of his company. With greater wealth, we can best help those around us, in addition to ourselves. So, it’s not just about money. It’s also about maximizing our ability to help others.

Focusing on the long term is much like educating our children. What you’ve already done for your children is what needs to be done for your company. Children don’t provide any meaningful output for at least the first 18 years of their life, and commonly 22 to 26. All that time and money during this quarter century is spent preparing a child for the workforce and life. His or her lifetime earnings and life satisfaction are dependent on this period of investment in their future. We are investing in human capital via training and education.

There are metrics that are proxies for how our children are doing during their first 18 years: their grades, number of intimate friends (an indicator of social skills), and participation in social activities including sports. These metrics give us an idea of how the child is doing and what their prospects are for the future, long before we start to measure their income and net worth. We can think of those as key performance indicators for measuring Intellectual Capital (the value of a company above the value of its tangible assets) and its creation. The time we spend with our child coaching them – guiding them – in known in our business as “Knowledge Management”, or the process of constant learning and improvement known as Kaizen in Japan.

Real shareholder value maximization is about the creation of long-term value. We study this in our work on Intellectual Capital. Research and Development – as but one example – is expensed on the income statement and reduces reported income. In reality, it increases the value of the company over the long run because it increases the company’s new products, or cost reductions. The use of GAAP accounting does not accurately reflect the accretion of value due to the R&D activities. Public companies attempt to make disclosures, but analysts are still challenged on knowing how to use the data. The investment in acquiring and training people is expensed from an accounting standpoint, when I reality is and asset that yields great returns.

Since our firm works predominantly with private companies, you would think that the owners always look out into the future and try to build the most value over the long term. That is not always the case. There are occasions where we see an absence of investment in talent acquisition, talent retention, and succession planning. Nothing destroys the value of a privately held business like losing its key man. Owners must acquire and retain their successor.

A lack of investment in Human Capital shows itself with an absence of job descriptions, a lack of performance reviews, and an absence of any of linkage to key performance indicators. This is paramount to flying in the dark without instrumentation, and it can have potentially fatal consequences.

We also see a lack of investment in keeping up to date with the technology of the industry. Few things stay the same in this world, given the rate of technological change. There needs to be a process for staying abreast of industry and technological changes.

This is barely scratching the surface of the issues that go into the subject. The time and effort invested in working towards the goal of maximizing shareholder value provide their own rewards in both the capital raising process, and in the exit planning phase of the mergers and acquisitions process when the owner decides to transition out of the company. If, however, the owner transfers ownership and operations to the next generation, the effort put into maximizing shareholder value becomes more apparent. These would include constantly looking for ways to improve the company, periodically re-engineering the company, re-accessing the customers and market segments the company serves, and reviewing its supply chain.

The challenge for the privately held business owner is that they get comfortable with their performance and stop having new ideas integrated into his process that can take the company to the next level. That is where we can help. To learn more, contact us

{kind=link}