|

Standby letters of Credit are perhaps the most misunderstood financial instrument in the world of credit. They are a direct credit substitute and take on the same risk as a loan, but they have their own language and few extra dimensions. They are used to arbitrage the difference in trust between the applicant (company) and the issuing bank.

SBLCs are a direct credit replacement and require that the relationship bank bear the risk of the underlying company or project. When studying a SBLC structure, it is imperative to first determine who is taking the underlying risk and the conditions under which they will take such risk. This will be outlined in a term sheet, and is the first and most important document to obtain.

SBLCs are commonly used as payment or performance guarantees. The bank which issues the standby letter of credit assumes the risk of the applicant of the letter of credit. The issuing bank will create a reimbursement agreement that is the parallel of a loan and security agreement which outlines the terms of the facility and its payment and default terms.

Drawings on a standby letter of credit generally do not require any proof of a lack of performance by the applicant. The Issuing Bank has no defenses to paying out under a draw request, which is usually accompanied by a simple statement by the beneficiary that a certain event has occurred.

A stand-by letter of credit can be used in a variety of ways:

• allow a customer to create rapport with a supplier by showing that it can fulfill its payment obligations

• to ensure fulfillment of a contract

• secure payment for goods delivered by third parties.

• to guarantee repayment of loans

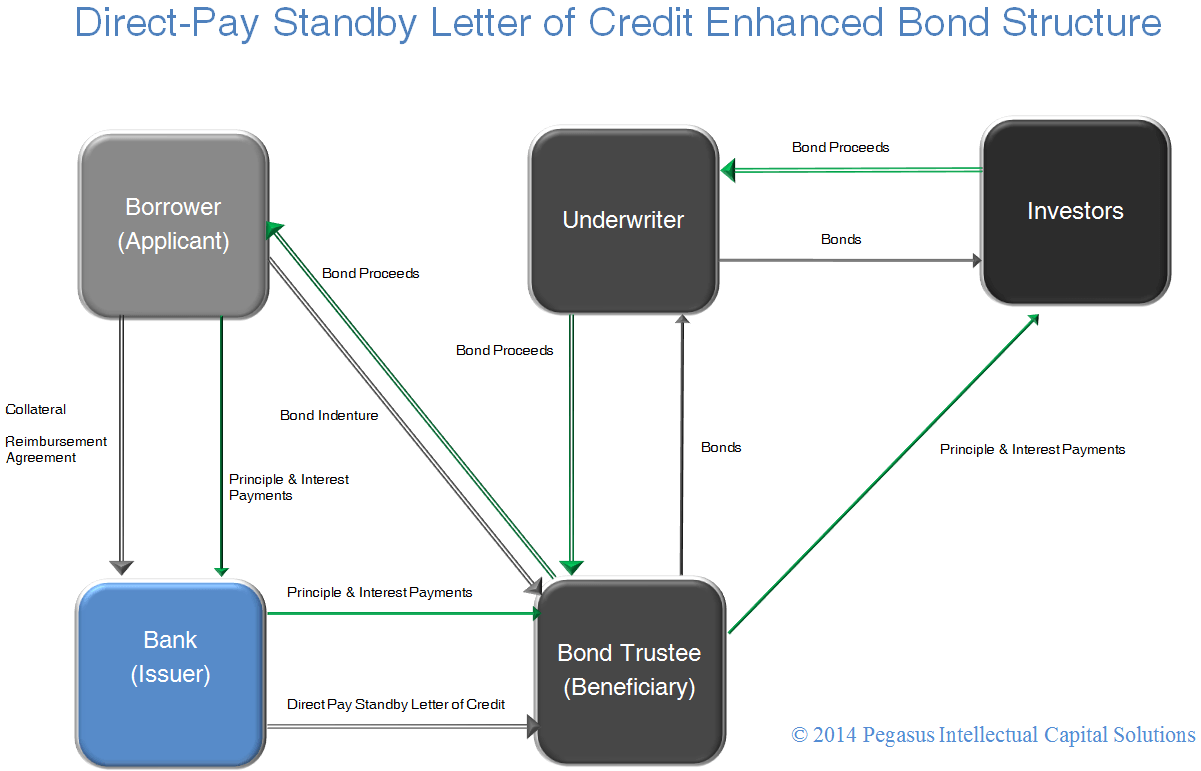

• to guarantee payment of interest and principal to a bond trustee

Direct-Pay SBLCs can be used to back the issuance and payment of bonds, including lower floaters (weekly reset bonds), MTNs (medium term notes) and longer term bonds. They are used by both corporations and in project finance. If the Issuing Bank does not have a credit rating which supports the needs of the bond market, the Issuing Bank can have its letter of credit confirmed by an investment grade Correspondent Bank.

The Issuing Bank assumes the risk of the company or project, and the Correspondent Bank assumes the risk of the Issuing Bank. The bond holders, via the bond trustee, receive all payments through the Confirming Bank/Issuing Bank ), effectively isolating the bond holders from all credit risk of the company or project. This permits the bonds to be rated by one of the rating agencies. This is a cost-effective way to raise capital when the financing is roughly $20mm or greater. The bond can be increased at anytime thereafter subject to the approval of the Issuing Bank, thus levering the costs of the original legal and underwriting costs of the first tranche.

Stand-by letters of credit are generally less complicated and involve far less documentation requirements than documentary (trade) letters of credit. They are used primarily in the United States and are governed by International Chamber of Commerce (ICC), and Uniform Customs and Practices (USP).

For more see:

|

{kind=link}