|

Capital structure decisions are dictated by the market. A company’s decision to finance with any particular financial instrument is determined by the market’s demand. And that demand shifts with changing appetites for any sector, company size, technology, product, or customer.

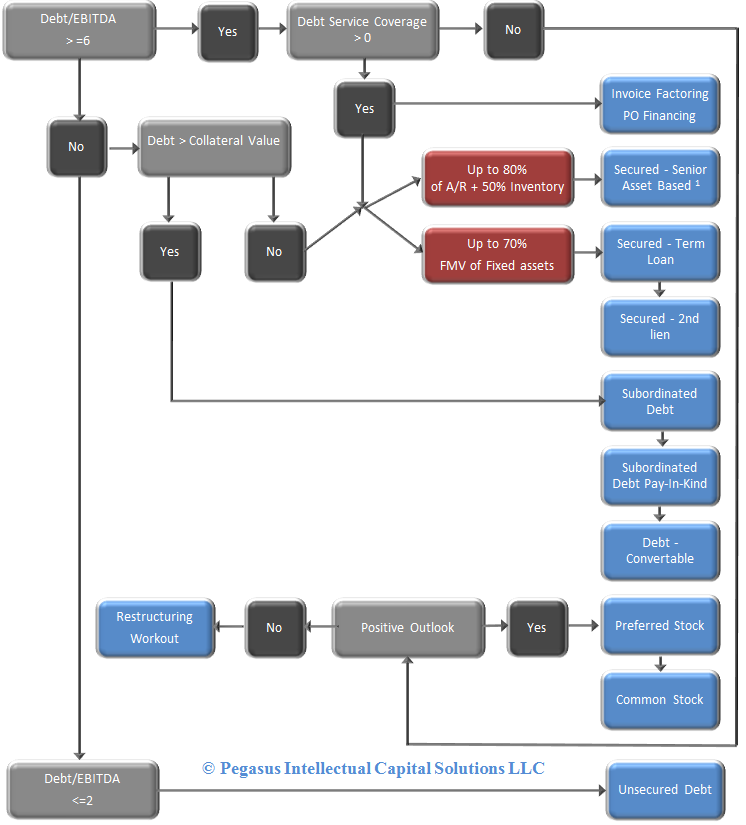

New capital maintenance rules limit the range of companies that banks can lend to. “Probability of Default”, or PD, is a metric that is determined by black box credit models, such as Moody’s KMV. In addition, Basel II, and III require the calculation of “Loss Given Default”, or LGD. The product of these two metrics is the expected loss on a loan and equals the loss reserve (capital) that the bank is required to maintain (and charge for). The consequence is that any company that is small, leveraged, in a cyclical or volatile industry, that lacks tangible assets for collateral, will struggle to obtain bank financing.

With the advent of stress-tests for banks, the corollary is that banks will test the loans in their portfolios for the same stress. All companies will need a diversified customer base (all customers at less than 10% of sales), definable, mitigateable risks, and have several years of operating history.

Shopping for a bank will become increasingly less fruitful. The imposition of standardized metrics and stress-tests on all banks will create a nearly universal lending policy across the industry. If you are a middle-market manufacturer or distributor, you will need to have less than 4-5 times total Debt/EBITDA, receivables, inventory and/or fixed assets as collateral under standard advance rates, and be able to sustain a 1.25 Debt Service Coverage under a stress-test. Service companies will generally need to be inside of 2x Debt/EBITDA.

If you are a Knowledge Era company, you will need non-bank financing. The stability and certainty of cash flow becomes the primary credit metric, along with size and age of the company. If you are in the process of building a company, mapping out the growth plan will aid in your exit, as financing will be available for the buyer.

For more see:

|

{kind=link}